Updated Tuesday 19 May 2026.

Premium updates for 2026-27

For all policies issued or renewed on or after 30 June 2026.

Workers Compensation premium rates for 2026-27

The Workers Compensation Legislation Amendment (Reform and Modernisation) Act 2026 introduces a premium rate freeze for 26-27 and 27-28.

The 2025-26 Workers Compensation Industry Classification (WIC) rates will be maintained for the 2026-27 policy period.

Premiums may still change due to:

- changes in wages

- changes in business activity

- an employer’s own claims experience.

- incentive eligibility.

Further details on WIC rates are available in the Frequently Asked Questions below.

Minimum premium

The minimum premium payable for a policy will remain at $240.

Experience-rated capping

To help maintain stability, premium-increase capping for experience-rated employers will reduce from 30% to 25%.

Employer-paid claim excess

The reforms introduce an excess that employers must pay at the start of a claim. In response to this, the cost of an individual claim for premium calculation purposes may be reduced by any employer-paid excess amount.

Loss Prevention and Recovery Plus

icare have introduced a maximum premium of 5.985 x Average Performance Premium (APP) for LPR Plus policies, providing greater certainty for participating employers.

Safe Employer Reward (SER)

Introduced 30 June 2025, but effective from 30 June 2026, SER eligibility includes timely submission of actual wages declaration forms for prior policy periods (in addition to existing performance criteria).

Visit the Declaring wages page for further information and support.

Frequently Asked Questions

These Frequently Asked Questions (FAQs) answer common questions about Workers Compensation premiums.

- Why has my premium changed under a premium rate freeze?

- What are Workers Compensation Industry Classification rates (WICs)?

- How will the premium capping change impact employer premium?

- How will the excess change impact employer premium?

- What is the Safe Employer Reward (SER), and what has changed?

- What can employers do to help reduce their premiums in future years?

- What options do employers have if they cannot pay their premium in full?

- What are Wage Declarations and why are they important?

- What happens if I don't declare my wages?

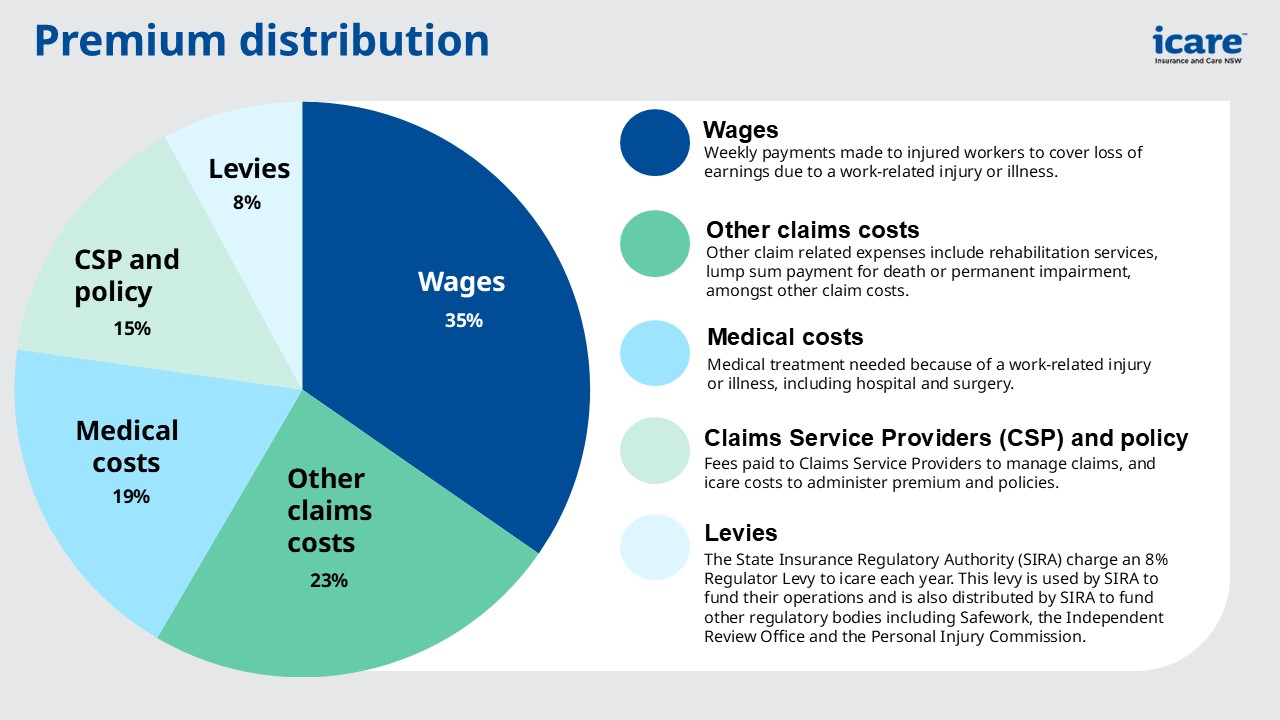

- How is my premium distributed?

- How do I know if my business is eligible for the Loss Prevention and Recovery (LPR) or LPR Plus products?

- Where do I go if I have questions?

{kind=link}

Premium review or disputes

We understand you may have questions about your premium. We are here to help.

What can you do?

Contact your Policy Team directly, or on 13 44 22. Here’s what you can expect from the support we provide:

Understanding and guidance

- If you don’t understand how your premium was calculated, we’ll go through the details with you and explain it in plain language.

- We will check we that we have the correct information about your business

- If you need help with paying premium, we can arrange for a premium collections team member to reach out to you to discuss a payment plan.

Timeframes

- If we can’t help you on the spot, we’ll let you know how long it’s likely to take. In most cases, this will be between five and 21 business days.

- You will be given a case number to use when contacting us.

- We will stay in touch and let you know if there are any delays.

How we resolve premium disputes

We use a consultative dispute process which means we work with you to resolve issues.

During this process:

- We’ll provide guidance to all parties involved on what information we need

- We’ll explain what actions are required to helps reach a resolution.

- We’ll keep you informed of our progress.

If your premium concern can’t be resolved and you need to move to a formal appeal*, we will start that for you and help you through that process.

*Formal appeals are used when the calculation of your premium is correct, but you feel other factors were not considered or the calculation doesn’t meet SIRA's Premium Guidelines.

What we need from you

- We’ll let you know at the start of your review exactly what information we require.

- We ask that you provide us with this information quickly, so we can resolve the issue as efficiently as possible.

Helpful resources

- Expression of Interest - Loss Prevention and Recovery (LPR) Product 0.12 MB(pdf)

- Loss Prevention and Recovery Statement of Product 2026-2027 0.38 MB(pdf)

- Loss Prevention and Recovery Plus Statement of Product 2026-2027 0.34 MB(pdf)

- Loss Prevention and Recovery Premium Model Guidelines 2025-2026 0.88 MB(pdf)

- Loss Prevention and Recovery Plus Guidelines 2025 0.52 MB(pdf)